A debt elimination plan is a methodical process that people and companies can use to gradually pay off their obligations and become financially independent. Reducing and eventually getting rid of existing debts—, which could include loans, credit card bills, and other financial obligations—is the main objective.

Evaluating the existing financial condition is the first stage in developing a debt elimination plan. This entails creating a list of all obligations, indicating interest rates, and being aware of the monthly payment obligations. After the total debt landscape is known, people can rank their debts according to interest rates, remaining sums, and terms provided by their creditors.

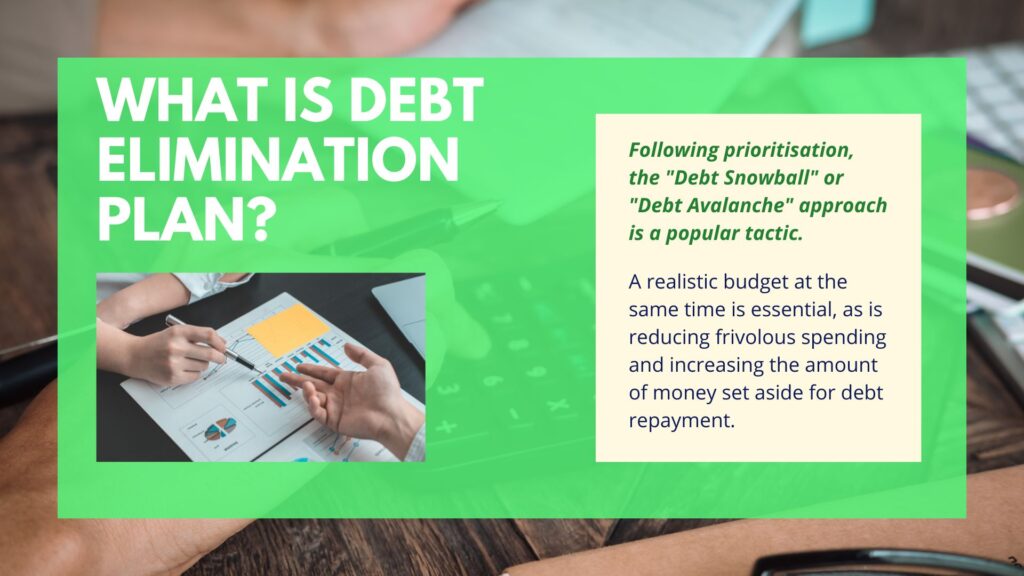

Following prioritisation, the “Debt Snowball” or “Debt Avalanche“ approach is a popular tactic. By paying off the lowest bills first, the Debt Snowball method gives people a psychological boost when they realise early gains. In contrast, the goal of the Debt Avalanche is to reduce total interest payments by concentrating on high-interest obligations.

Making a realistic budget at the same time is essential, as is reducing frivolous spending and increasing the amount of money set aside for debt repayment. Making payments on time each month and avoiding taking on new debt are crucial elements of a successful debt elimination plan.

Some people might look into debt consolidation programmes, which combine several loans into one easier-to-manage loan with possibly reduced interest rates. It is also advisable to seek professional guidance from debt management agencies or financial counsellors.

Regular monitoring and plan modifications may be required along the process, particularly in reaction to unforeseen expenses or changes in income. Rewarding yourself for reaching milestones helps keep you motivated.

In the end, a debt elimination plan is a customised road map for achieving financial independence, providing a disciplined and organised method to eliminate debt and create a more stable financial future.