PB Fintech is well known as Policybazaar.com and Paisabazaar.com. In this informatory mail including analyses of crucial key metrics (industry tailwinds and headwinds, business model, financial performance) which an investor looks at before subscribing to an IPO. The IPO details are as below:

| IPO Details | |

| Issue Size | Rs. 6017Cr |

| Fresh Issue | Rs. 3750Cr |

| Offer for Sale | Rs. 2267Cr |

| Listing at | BSE & NSE |

Objective of the issue

PB Fintech ltd, plans to raise for Rs. 6017Cr through fresh issue as well as Offer for sale (OFS). The sum raised through OFS where the amount will be distributed among the existing selling shareholders and the company won’t receive anything. It is raising a greater sum through the fresh issue, and it intends to use the net proceeds towards the following:

1) Improving brand image of Policybazaar, and Paisa bazaar & others:

PB Fintech Ltd. carries out many paid marketing strategies to get new clients. Of the total net proceeds, the company plans to use Rs. 1,500cr for coming marketing initiatives over the next three financial years.

2) Opportunities to expand consumer base and physical presence:

Policybazaar.com was just a multi-brand web-aggregator for insurance products. Now it has a license from IRDAI to be a “direct (life & general) insurance broker. This stages the ambitious plans of expansion of the company with its bouquet of products and services and improve their physical presence. PB Fintech Ltd. In this regard expects to use a sum of Rs. 375cr for settling and operating tangible retail outlets through FY24. By the end of July 2021, PB Fintech has 15 physical offices and plans to reach to a sum 200 outlets by FY24.

3) Funding strategic investment and acquisition:

PB Fintech Ltd. Is planning to enhance its services via investments in health and wellness sectors. To bring this into reality, PB Fintech aspires to use Rs. 600Cr for prospective acquisitions and strategic enterprises.

4) Funding international expansion plans:

PB Fintech has experienced its business grow with time, coherence to the business model they follow. The company intends to reproduce the same scalable model and expand in economies outside India. Middle East and South East Asia are the company’s likely future destinations. Currently, PB Fintech has functioning in Dubai through a subsidiary PB Fintech FZ – LLC. The company intends to use Rs. 375cr for potential global business expansion.

5) General corporate Purposes:

Any balance left out of the net-proceeds will be used towards general corporate purposes such as investment in subsidiaries, working capital needs, salaries, wages, rent, administration expenses etc.

Understand the Business

PB Fintech Ltd. is a unicorn FinTech startup co-founded by IIT graduate Yashish Dahiya and IIM graduate Alok Bansal, in 2008. It trades via internet platforms, Policybazaar.com and Paisabazaar.com

Policybazaar is the India’s largest online insurance platform constructed for consumers and Insurers buy and sell core insurance products respectively. As of March, 2021, 51 insurer partners have prospected more than 340 home, term, travel, health, and motor insurance plans on Policybazaar.com. This shows a substantial portion of all licensed companies in India. In FY21 alone, over 48mn users registered on Policybazaar.com and have purchased more than 19mn policies from listed insurer partners.

It’s a one-stop platform for pre-purchase research, purchase, inspection, medical check-up, payment, post-purchase policy management, including cancellations and refunds.

PB Fintech’s launched its second platform, Paisabazaar in 2014 with a vision to ease lending for a significant portion of Indian population. According to analysts, Paisabazaar based on disbursals, is India’s largest digital consumer credit marketplace with a 51.4% market share, in FY20. The widely used feature of Paisabazaar is CIBIL/credit score checker, as 21.5 million users have accessed their Credit score through the platform.

It’s an independent & innovative digital lending platform that allows users to compare, choose and apply for personal credit products. It has 54 partnerships with large banks, NBFCs and other FinTech lenders. These entities offer a wide choice of product offerings across categories including personal loans, business loans, credit cards, home loans and loans against property.

Who’s selling?

The sum will be raised through fresh issues, PB Fintech Ltd. is raising Rs. 2267cr through OFS. Founder and CEO Yashish Dahiya and Co-founder and director Alok Bansal are discharging shares up to Rs. 250cr and Rs. 95Cr respectively. Other selling shareholders include Founder United Trust, Shikha Dahiya and Rajendra Singh Kuhar, they are selling shares aggregating up to Rs. 27.5Cr, Rs. 12.5Cr and Rs. 7.5 Cr each. Investor shareholder, SVF Python II (Cayman) Ltd. is offloading shares worth Rs. 1,875Cr.

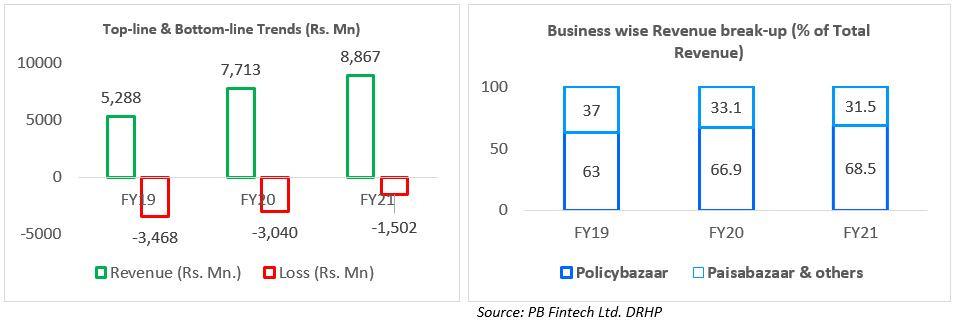

Story through charts

- PB Fintech Ltd.’s income has been touching sky regularly, however, the company has not yet posted profit.

- On the other hand, losses have been decreasing continuously. In FY21, the losses reduced to Rs. 1,502Mn from Rs. 3,468Mn in FY19. Other internet companies showed the similar trend.

- Policybazaar.com contributed 63%, 66.9% and 68.5%, to the total revenue. And the rest was Paisabazaar.com contribution in the financial years of FY19, FY20 and FY21 respectively.

- PB Fintech Ltd. generates revenue from the complete set of services. It urges on commission or fees from partners listed on both the platforms. It also deducts commission from the insurance premium payable through the platform. Additionally, it earns from outsourcing services, sale of leads, IT support services, rewards, online marketing and consulting, Tele calling services, human health services, Investment advisory fees, and Commission from online aggregation of financial products.

MyFinopedia’s Views:

PB Fintech has not yet posted profits; however, the company has promising platforms which consumers use regularly and want to continue using. Moreover, it has reduced losses year-after-after, similar to the industry trend of most internet companies. Thus, we can hope that the company can post profits in the future.

PB Fintech Ltd. operates its business in insurance and finance sector. Both these sectors are improving. Factors which favor the insurance sector includes, increase awareness among Indians due to the COVID-19 pandemic, and various government initiatives like PMJJBY & PMJAY etc. and the increased FDI limit from earlier 49% to 74%. According to Frost & Sullivan, the insurance industry in India can grow to US$ 520Bn. The consumer lending industry is expected to witness 9.1% CAGR to reach $1,041Bn by FY30.

On account of these theories, it’s secure to say that PB Fintech is in for a successful ride. Insuretech is getting propulsion with other players flocking the space. Talking about insurance web-aggregator, Policybazaar will be the only listed platform.

Disclaimer: Information shared in this email is only for educational purpose. One should not consider it as a buy/sell/hold recommendation by MyFinopedia. Giving free recommendations without assessing an investor’s risk is prohibited by SEBI.